We investigate the performance of two simple trading techniques versus investing in the market. In particular, we review momentum and countertrend betting in the US Growth Mutual Funds between 2018-2021 1. The purpose is to demonstrate, in terms of fairly simple examples, how various tactics and strategies can be compared using peak-to-trough recoveries.

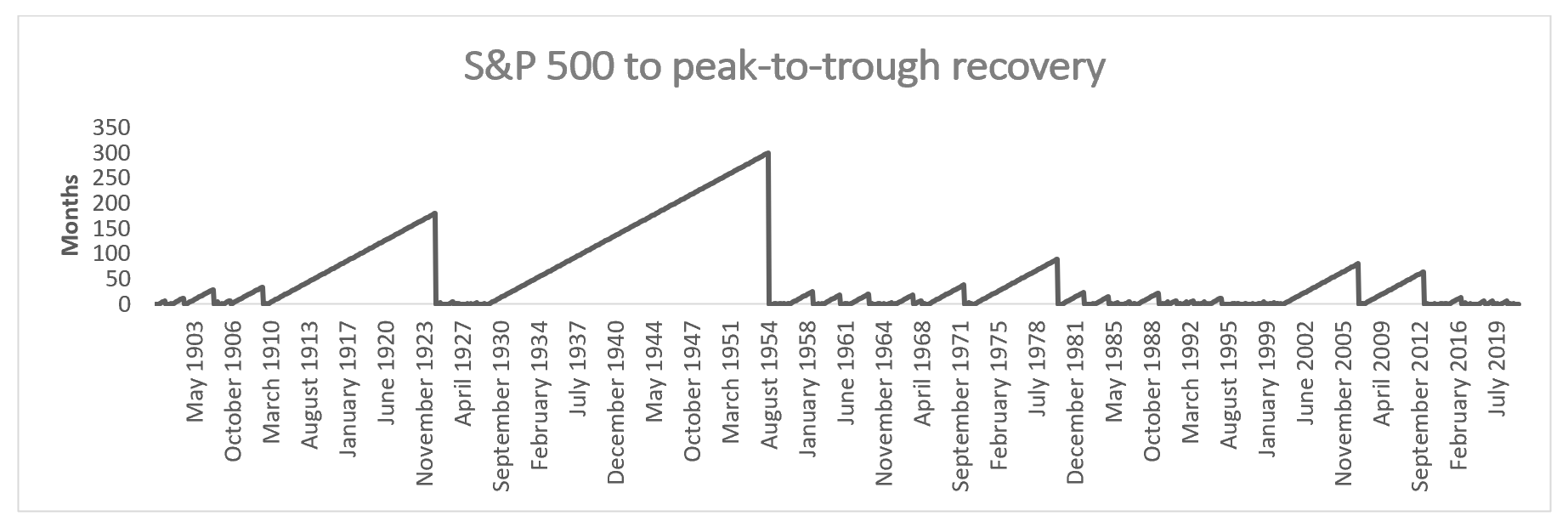

Buying at the top is the nightmare scenario for any investor. Purely from a probabilistic point of view, it is highly unlikely that the given asset or a fund is at its peak today. Yet, securities that are much (abnormally) discussed in the media are more exposed to this risk. We shall count how long (in months) it takes to recover from buying at the peak, i.e. peak-to-trough recovery duration. For example, since 1900, the average peak-to-trough recovery period for the S&P 500 is just about a year; the longest ever period being 299 months that took to reach pre-1929's Wall Street Crash highs (see Figure 1 2).

Figure 1

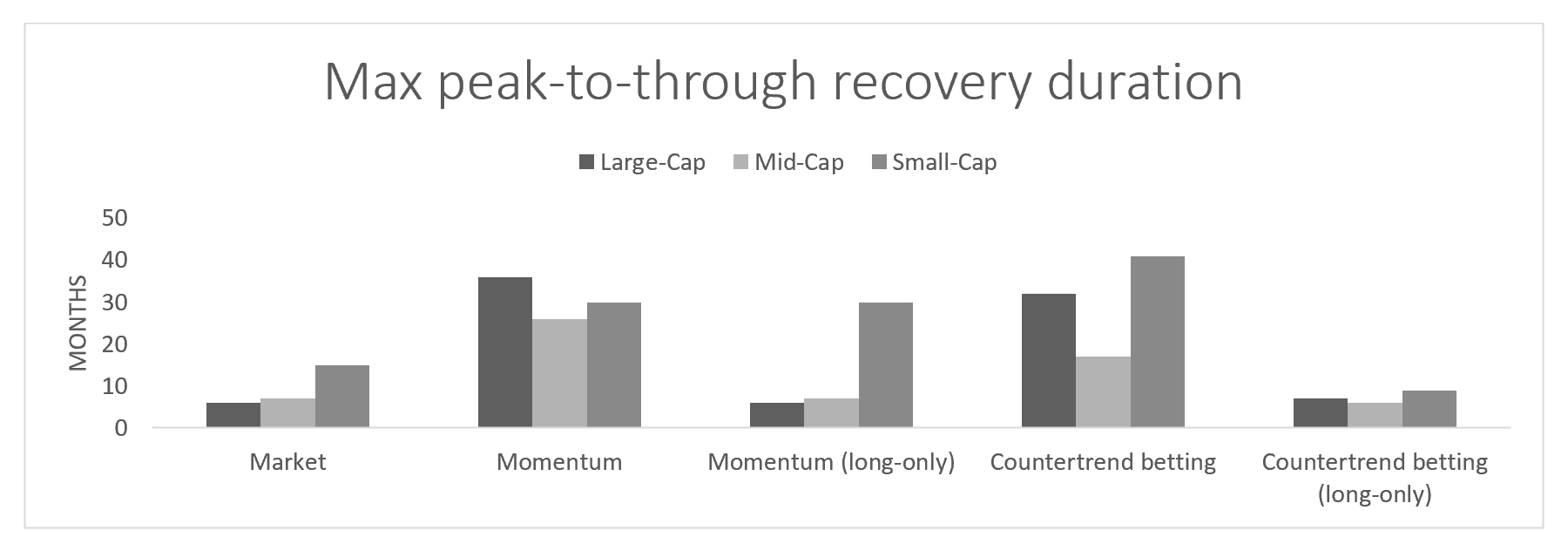

The first strategy is to buy or sell into the momentum of funds that have performed above or below average. We also consider the equivalent long-only strategy, where we avoid short positions*. The second strategy, countertrend betting, is to buy or sell into the underperforming/overheating funds (i.e. those whose performance is out of the range of two standard deviations from the average). Likewise, we have looked at the long-only equivalent. These strategies are compared to buying every fund in the market. For the period considered, large-, medium- and small-cap growth funds performed rather well; the total return was 98.32%, 88.80% and 86.46%, respectively with the annualised return of 21.61%, 19.91% and 19.48% and the standard deviation of 18.42%, 20.47% and 23.17%. Furthermore, the longest peak-to-trough recovery periods were 6, 7 and 15 months, respectively.

Out of the considered strategies, long-only significantly performed better than their "riskier" counterparts. However, it underperformed buying the market, with durations to recoveries more or less coinciding (except for small-cap funds, where it performed much better for countertrend betting and far worse for momentum strategy). The absolute returns, for long-only strategies, were within the margin of error of returns from buying every fund. Thus, if one ought to incorporate the corresponding fees associated with taking various positions, it would make such strategies rather unattractive. On the other hand, the strategies where we allowed for short positions, performed significantly worse, with negative or (at best) single-digit returns, and duration to peak-to-trough recoveries were (on average) 30 months (see Figure 2).

Figure 2

Based on the peak-to-trough recoveries, it appears that, at least in the case of the US Growth mutual funds, the considered strategies are sub-optimal, and risky if one allows for short-positions. Given that these funds (on the whole) performed rather well, it would be interesting to test them in more volatile periods.

1 Based on the analysis of 1334 star-rated North American Growth Mutual funds from Morningstar.

2 According to Yahoo Finance and DataHub as of 01/07/2021.

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003