We find that Modified Value-at-Risk (MVaR) Optimisation is a superior optimisation technique for Hedge Fund portfolios.

We will compare two portfolio optimisation techniques – Drawdown-Adjusted VaR Optimisation and MVaR Optimisation – to see which method gives us superior risk-adjusted performance. The optimization we conduct will be a 36-month rolling (6 month holding period) out-of-sample optimisation. We will use a randomized hedge fund dataset consisting of portfolios with track-records of 131 months.

MVaR Optimisation

Modified Value-At-Risk [Favre, Galeano 2002] is a VaR measure which accounts for skewness, kurtosis, and volatility in assets which exhibit negative skewness and/or positive excess kurtosis, for example hedge funds. The objective function in our optimisation is:

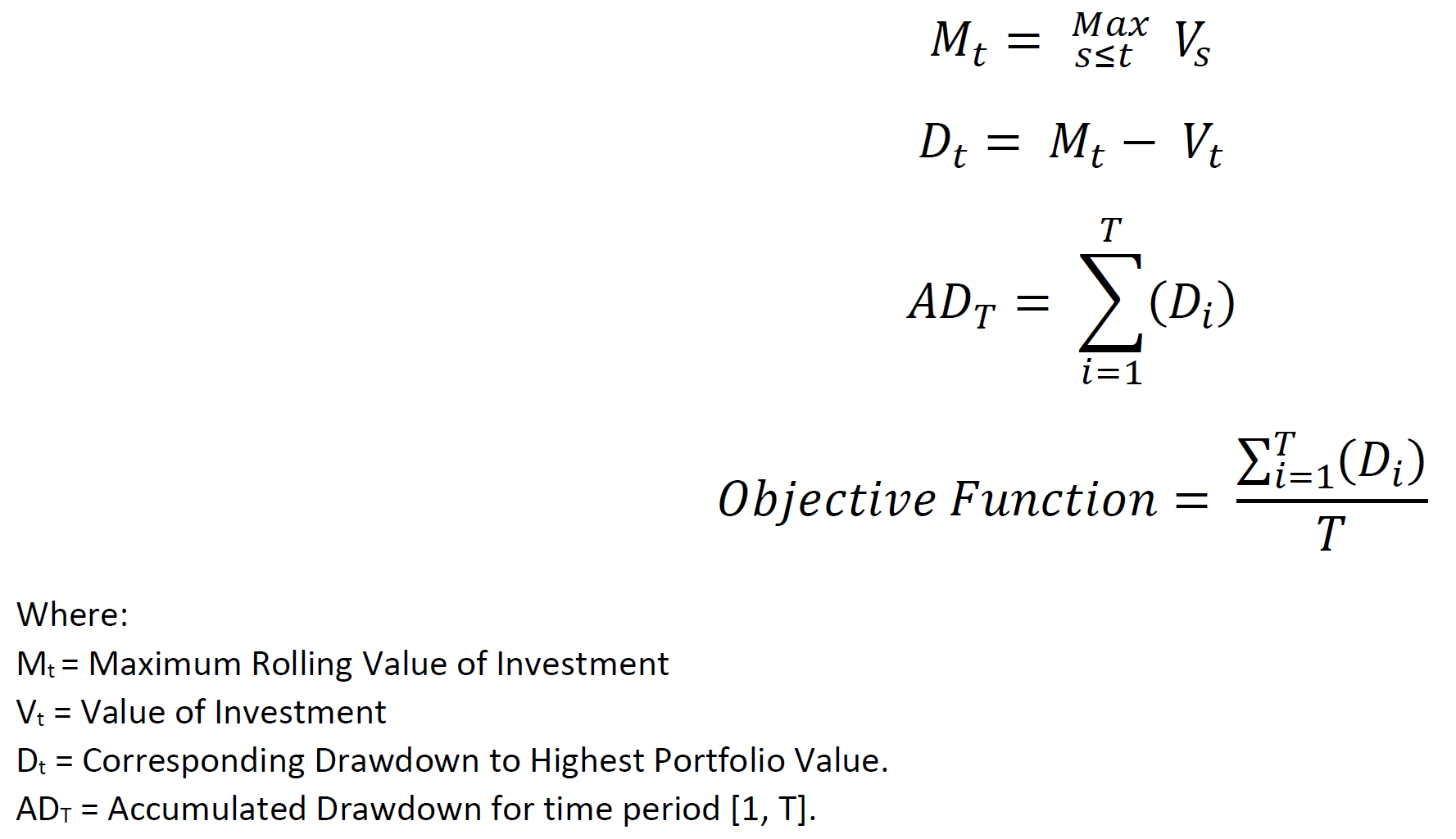

Drawdown-Adjusted VaR Optimisation

The technique we will use minimize the frequency of drawdowns and their magnitude [InvestSuite, 2019]. The idea behind this methodology is to find the rolling maximum value of the portfolio, its corresponding drawdown, the different drawdowns within a period T, and the sum of those drawdowns – accumulated drawdown. The objective function is the mean of the accumulated drawdown - seen below:

Results

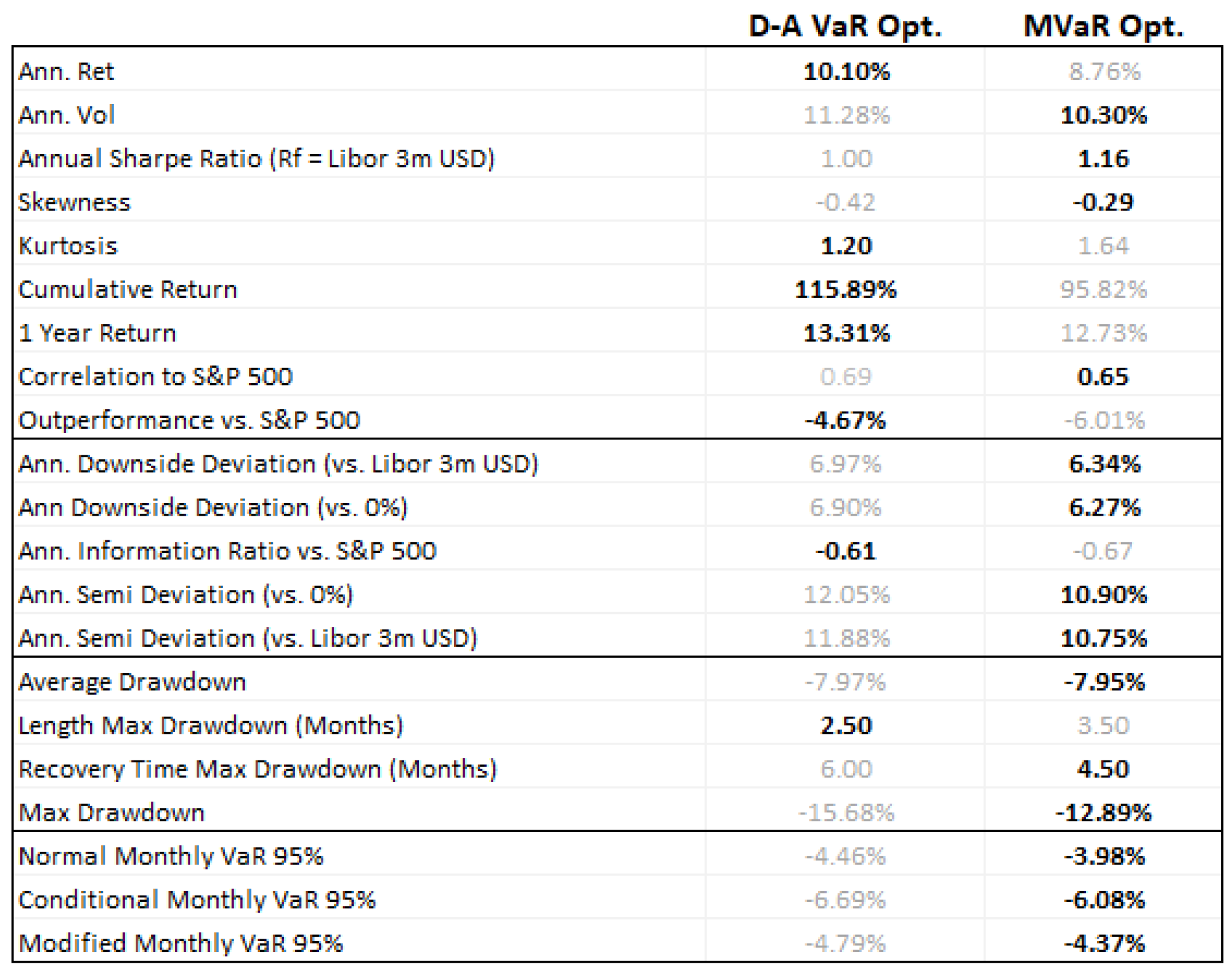

Table 1.0 Optimiasation Results

In Table 1.0 the results show the median values for each out-of-sample optimisation technique. MVaR Optimisation provides superior risk-adjusted portfolios vs. Drawdown-Adjusted VaR Optimisation; MVaR also outperforms with respect to drawdown statistics. However, the cumulative and annualized returns are superior for the portfolios created using Drawdown-Adjusted VaR Optimisation.

In conclusion, when creating portfolios with assets that have unique skewness and kurtosis characteristics, MVaR Optimisation is a superior technique to Drawdown-Adjusted VaR Optimisation. We can see portfolios created using this technique outperform on numerous portfolio level statistics and provide a superior Sharpe Ratio, VaR profile, and drawdown profile.

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003