We are halfway through 2021, and it is safe to say that value funds have had a tremendous run. Earlier this year, many analysts spoke about great value rotation 1 and when it will end. The meme stocks are still here, and SPACs could play a role (of a proverbial thermometer) in the market. The economy reopening, stabilisation of the domestic political situation (in the US) and Biden's Infrastructure Plan all point to an economic boom. But, a global supply chain squeeze, micro-chip shortage, general inflation expectation (will they/won't they) and yet another (COVID) variant may temper the current momentum.

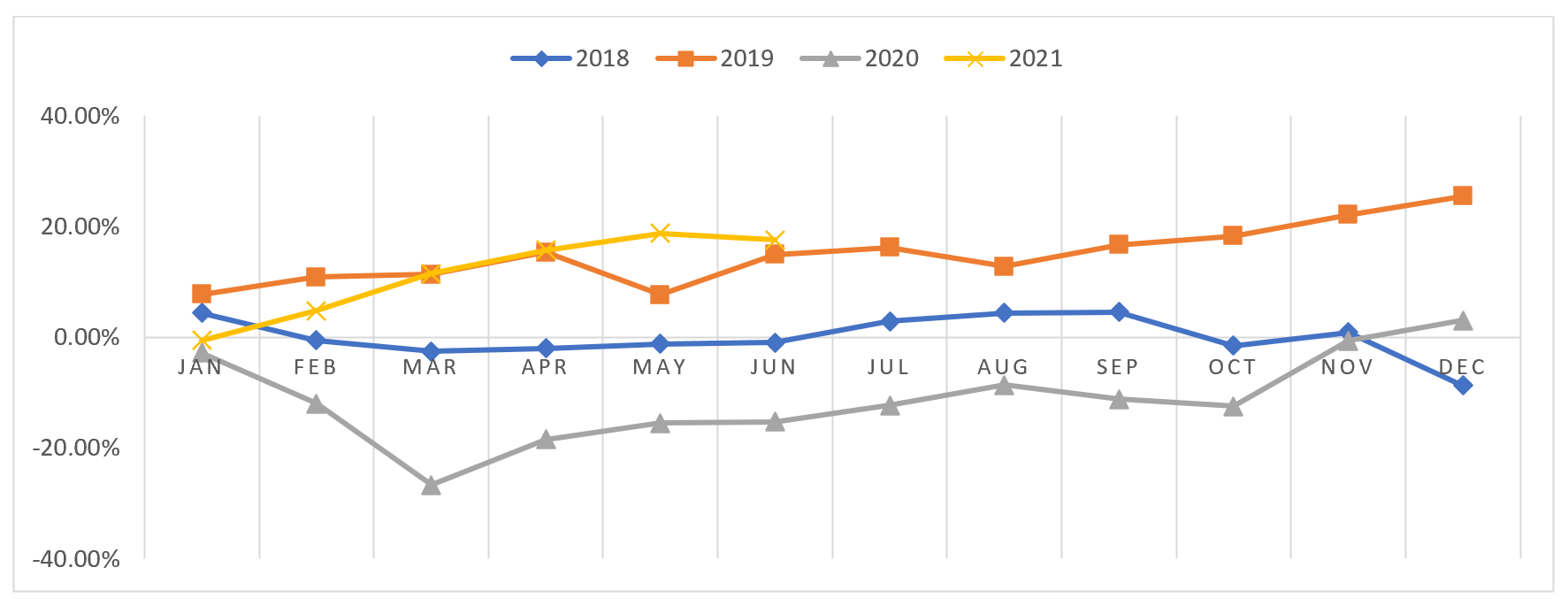

According to the Morningstar data 2 , since the beginning of the year, small, mid-cap and large funds have returned 28.48%, 21.71% and 17.61%, respectively, compared with 16.91% and 14.26% year-to-date returns of Russell 2000 and S&P 500 indices 3 . The last time we saw comparable gains in value funds was in 2019. Then, small, mid-cap and large value funds ended that year with 22.59%, 25.74% and 25.46%, respectively, outperforming the S&P 500 index (22.38% 3 ). Bridgeway Small Cap Value Fund (BRSVX) is the best performing value fund in 2021 so far, being up 55.77% to date. More than half of its portfolio is allocated to financial services, industrials and consumer cyclicals.

Figure 1: Cumulative returns of large value funds

By contrast, growth funds are within the range of what we have seen in the last four years. From January, small, mid-cap and large growth funds have grown by 12.58%, 10.02% and 11.71%, respectively (see Fig. 2). The deviation of returns between different funds is also wider compared to value funds, which were predominantly all (>99.7%) up this year, while some 4% of growth funds considered are down. The best performer among the growth funds so far is Kinetics Spin-Off and Corporate Restructuring Fund (LSHAX). It is 63.81% up in 2021. The fund is heavily invested in the energy sector (more than 60%).

Figure 2: Year-to-date returns

In early May, Lou Miller of Goldman Sachs' Global Market spoke 4 about rotation from growth to value stocks driven by the successful vaccination program (in the US) and reopening of the economy. Many analysts 1 believe that by the end of 2021, growth stocks should regain their dominance. "Mutual funds are overweight value to a larger degree than any time in our eight-year data history" according to Ben Snider and David Kostin (1). Value stocks are sensitive to the performance of the economy, and forecasted economic growth should peak at Q2, with the last two quarters averaging 7%, according to the Goldman Sachs Global Investment research 5 . This does not scream the death of value. Nevertheless, all else being equal, it creates an exposure to unforeseeable shocks to the market and the economy..

In conclusion, this year definitely delivers on a variety of investing themes. Value mutual funds greatly outperformed growth so far this year. But many believe that growth funds could have a better second half, and value-growth performance gap normalising and reverting to the historical proportions.

1 "The great value rotation in the stock market may already be over as investors embrace tech again" by Bob Pisani http://www.cnbc.com/2021/06/11/the-great-value-rotation-in-the-stock-market-could-be-over-already-as-investors-embrace-tech-again.html

2 Based on the analysis of 2480 star-rated North American Mutual funds from Morningstar.

3 According to Yahoo Finance as of 29/06/2021.

4 "From Growth to Value: Where We Are in the Equity Markets" http://www.goldmansachs.com/insights/pages/from-growth-to-value-where-we-are-in-the-equity-markets.html

5 "Roaring Reopening Trade Threatened With Boom Nearing Peak" https://www.bloomberg.com/news/articles/2021-04-23/roaring-reopening-trade-threatened-as-growth-cycle-seen-at-peakequity-markets.html

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003