The common aim of an investor is to maximize the return on their investments while minimizing risks. Reward-to-risk ratios are used to simultaneously achieve these goals. The most common Reward-to-risk ratio is the Sharpe ratio. Another variation is the Sortino ratio. The Sortino ratio differentiates between upside and downside volatility by using the standard deviation of fund returns below a specific minimum acceptable value. This form of standard deviation is known as Downside deviation.

As downside deviation focusses only on the negative deviation of a fund’s return from the minimum acceptable value, it gives a more accurate view of a fund’s risk as upside volatility is generally seen as an advantage. Consequently, the Sortino ratio is regarded as a better view of the fund’s risk adjusted performance versus the Sharpe ratio; especially in cases where the fund has high volatility.

As is the case with the Sharpe ratio, the higher the Sortino ratio the higher return premium per unit of risk, i.e., higher is better.

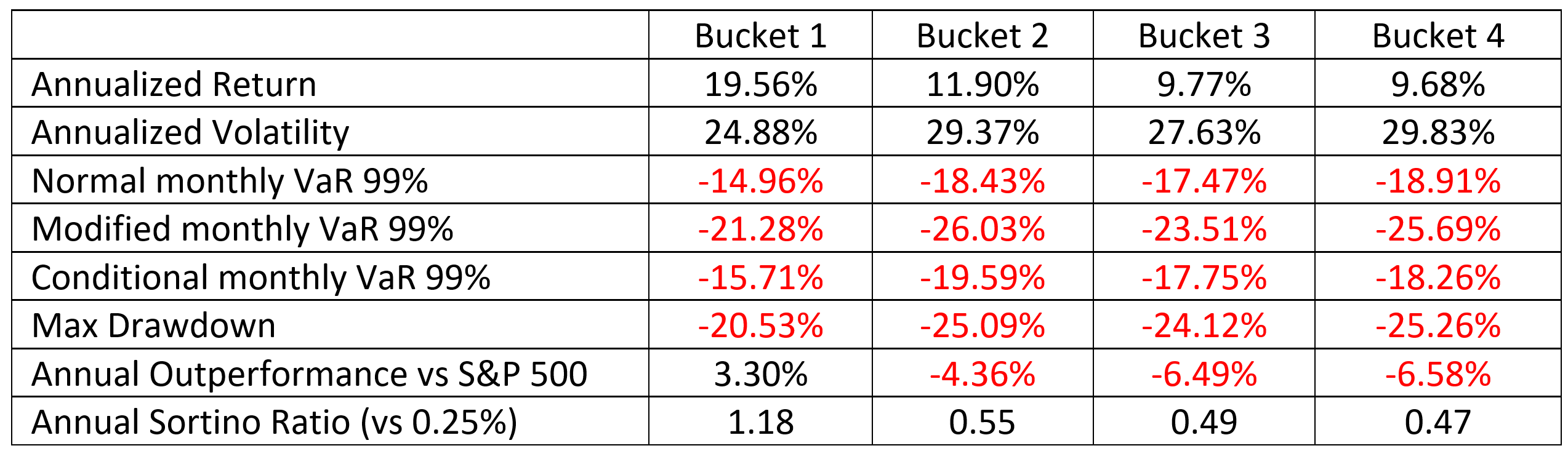

To demonstrate the power of the Sortino ratio, we will create a universe of high volatility hedge funds (funds with Annualized volatility over 20%). We will calculate the Sortino ratio (with a minimum acceptable return of 0.25%) between Jan 2005 and Dec 2019 (in-sample range) for each fund in the universe. The universe will then be divided into 4 quartiles based on Sortino ratio. Each bucket is displayed below.

Each bucket’s underlying funds are equally weighted. We then compute the risk and performance statistics out of sample during 2020, results are shown below.

Source: HFR, HFM, Eurekahedge

As you can see Bucket 1 outperforms the other buckets in terms of risk and return. There is a clear indication of when high Sortino ratio funds are selected we achieve better risk and return profiles out of sample.

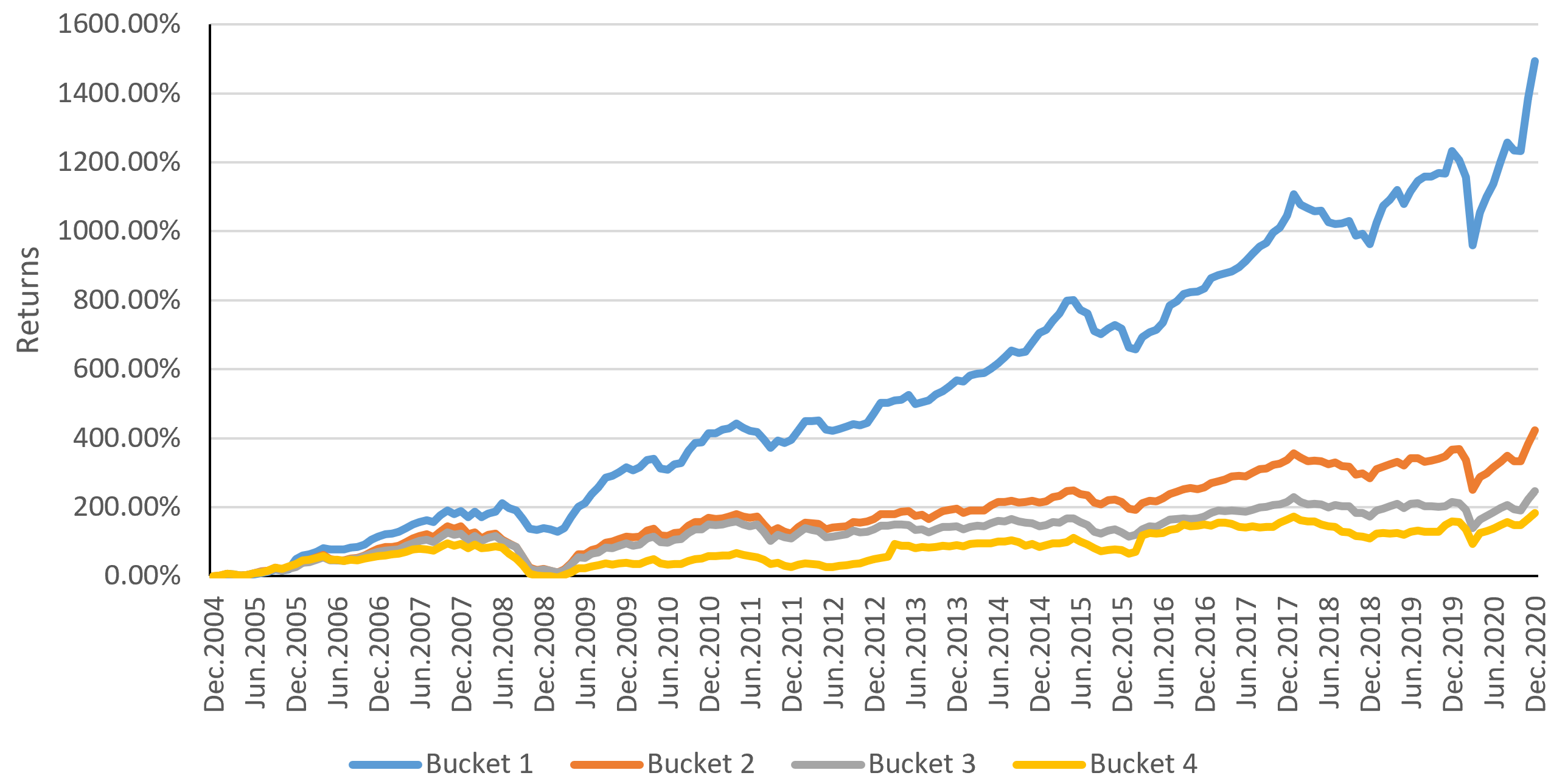

The total cumulative return for the full period for each bucket is plotted below. This demonstrates further that bucket 1 is the clear leader.

Conclusion

Sortino ratio is a very useful risk adjusted performance measure especially among high-volatility funds. We have demonstrated that selecting funds with higher Sortino ratios generally lead to superior out of sample performance both in terms of risk and returns. However, we must be aware of survivorship bias relating to fund data as well. Funds which have higher volatility typically may be excluded when performing fund screening exercises based on Sharpe ratio. Some of these funds might actually have upside volatility and provide additional benefit and thus using the Sortino ratio will make sure such funds are not overlooked. Again, it is recommended that you use your own judgement when deciding which Reward-to-risk ratio you would like to use.

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003