We find that skewness can be a useful metric for predicting future returns when looking at (North American) Equity focused Mutual Funds.

In this short article we aim to ascertain if negative skewness is a useful indicator of future returns in Equity focused Mutual Funds. We have taken the returns for North American Mutual Funds (AuM >= $1bn) starting in the year 2000 up until May 2021 (n = 1,200). From this data we have isolated the returns between 2000 and 2010 for each asset and grouped them based on their skewness into the following categories:

The basket weights were determined by AuM weightings. Each basket was then analysed for the subsequent period Feb 2010 – May 2021 to see if the historically positively skewed basket outperformed the negatively skewed baskets. There is more granularity on the negatively skewed portfolios as we tried to maintain reasonable basket sizes. We would expect that skewness would have some predictive capabilities with regards to future returns, however, skewness means little when we do not also factor in kurtosis; we must also account for the equity risk premium.

Results

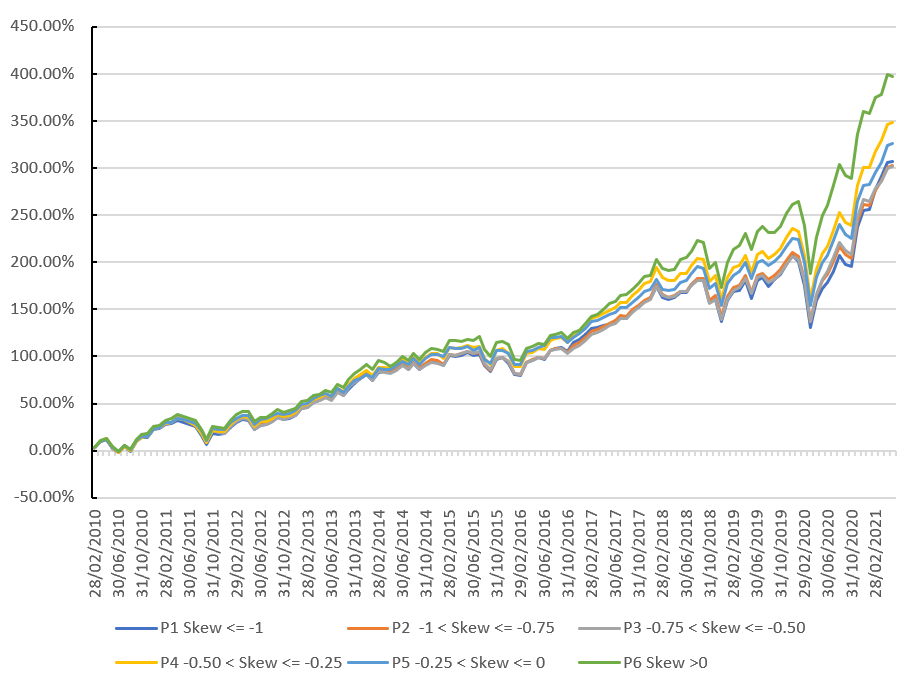

Figure 1.0: Basket Cumulative Performance Feb 2010 – May 2021.

The cumulative portfolio results, shown in figure 1.0, show that the basket constructed based on asset positive skewness seems to significantly outperform the negatively skewed baskets. Portfolio 6 had a cumulative return of 396.98% in the period, 325.82% for Portfolio 5, 347.84% for Portfolio 4, 301.11% for Portfolio 3, 302.31% for Portfolio 2, and 307.17% for Portfolio 1.

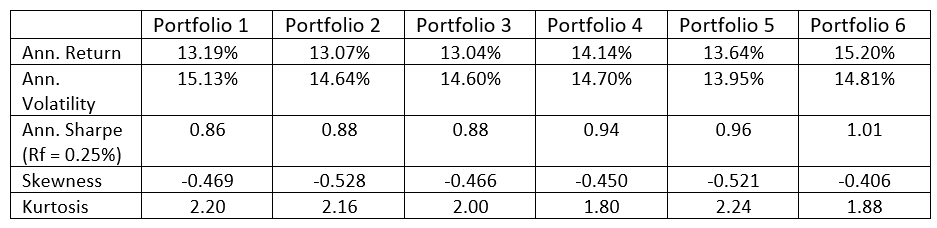

Table 1.0 Portfolio Statistics Feb 2010 – May 2021.

Table 1.0 shows that, on a risk adjusted basis, Portfolio 6 also outperforms the other portfolios. This portfolio exhibits a Sharpe Ratio > 1 and higher skewness and kurtosis than the other portfolios. A trend can be seen where the risk adjusted portfolio performance improves as we tend towards the less negatively skewed baskets. Positive skewness would suggest that each asset in the portfolio has a higher probability of extreme positive returns over negative ones.

In conclusion, we have determined that, for North American Mutual Funds, skewness can be a useful indicator of future performance based on historical data. However, we must be aware of the survivorship bias relating to fund data as well as the fact that one should always account for the kurtosis of a returns distribution when analysing skewness.

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003