It’s known that during crisis periods correlation between all assets increases substantially. In this article, we investigate if a hedge fund investor can keep their portfolio well-diversified during a crisis by investing across different strategies.

We selected 20 Hedge Fund Indices and built correlation matrix for them during two equal time periods. The first period is before the COVID-19 crisis, the second is starting with the COVID-19 crisis. Both period lengths are 18 months.

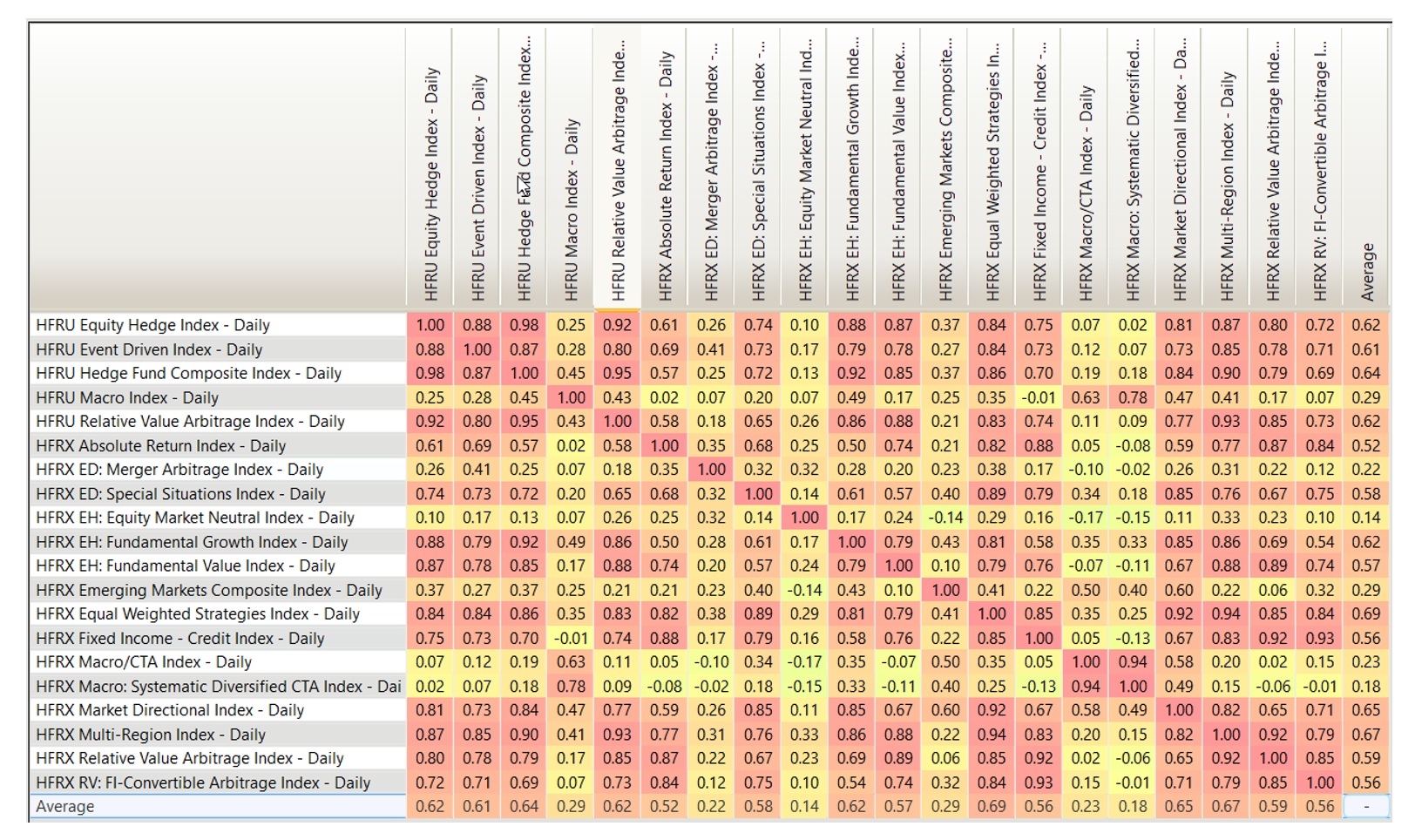

Table 1 - Correlation matrix for Hedge Fund Indices (Jul 2018 – Dec 2019). Average Correlation = 0.49

Table 1 represents pre-crisis period (Jul 2018 – Dec 2019). Overall average correlation is 0.49 with

being the best diversifiers by having the lowest correlation to the rest of Hedge Fund Indices.

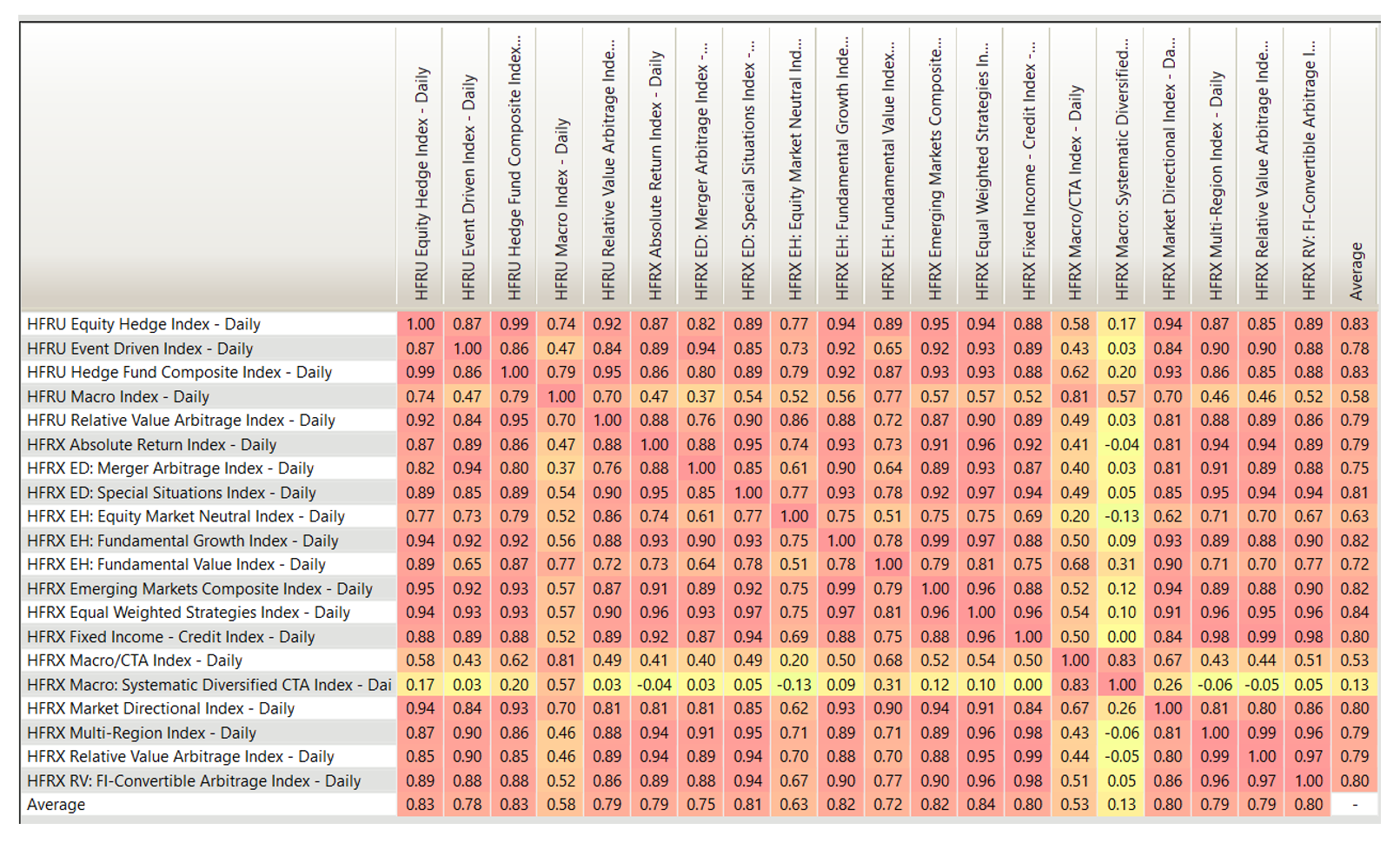

Table 2 - Correlation matrix for Hedge Fund Indices (Jan 2020 – Jun 2021). Average Correlation = 0.73

Table 2 shows that, starting from the COVID-19 crisis period (Jan 2020 – Jun 2021), correlations increase significantly giving overall average correlation of 0.73.

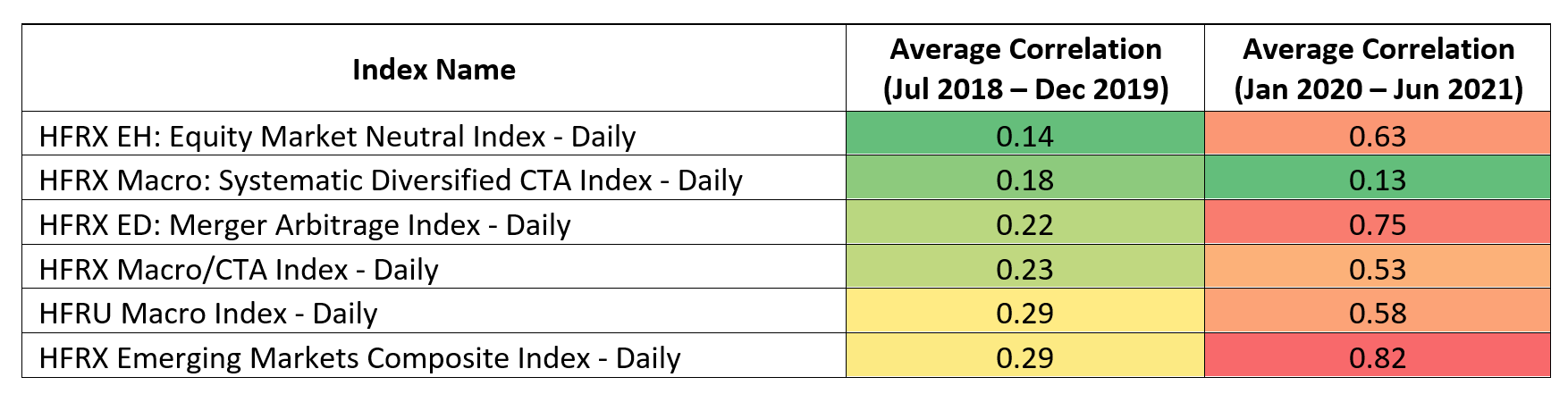

Table 3 – Average correlations comparison for the indices with lowest correlations before crisis.

Most strategies previously that were good diversifiers in the pre-crisis period saw their average correlations increase significantly with the onset of Covid-19. The only strategy which managed to keep its correlation low is HFRX Macro: Systematic Diversified CTA Index – Daily (was 0.18, now 0.13). Macro/CTA and Macro strategies can also be considered an acceptable diversification choice with correlations of their indices increased from 0.23 to 0.53 and from 0.29 to 0.58 respectively.

Emerging Markets and Merger Arbitrage strategies that seemed to provide diversification in normal market conditions failed to do this during the crisis with correlations increasing from 0.29 to 0.82 and from 0.22 to 0.75 respectively.

Conclusion:

A portfolio of hedge funds with different strategies may indeed look well diversified in normal periods, but hedge fund investors should keep in mind that diversification among strategies can be vulnerable. During times of crisis, correlation among hedge fund strategies increases. To have a higher probability of avoiding large portfolio drawdowns, investors should perform stress testing and consider including other asset classes in the portfolio.

N.B. This article does not constitute any professional investment advice or recommendations to buy, sell, or hold any investments or investment products of any kind, and should be treated as more of an illustrative piece for educational purposes.

To trial a truly powerful and comprehensive analytic software for investment decisions, fund allocation, and our new, innovative digital due diligence visit alternativesoft.com , call us on +44 20 7510 2003, or email us information@alternativesoft.com

71 Carter Lane, London

EC4V 5EQ

+44 20 7510 2003