From classic mean-variance to modern risk parity - every methodology your investment process needs.

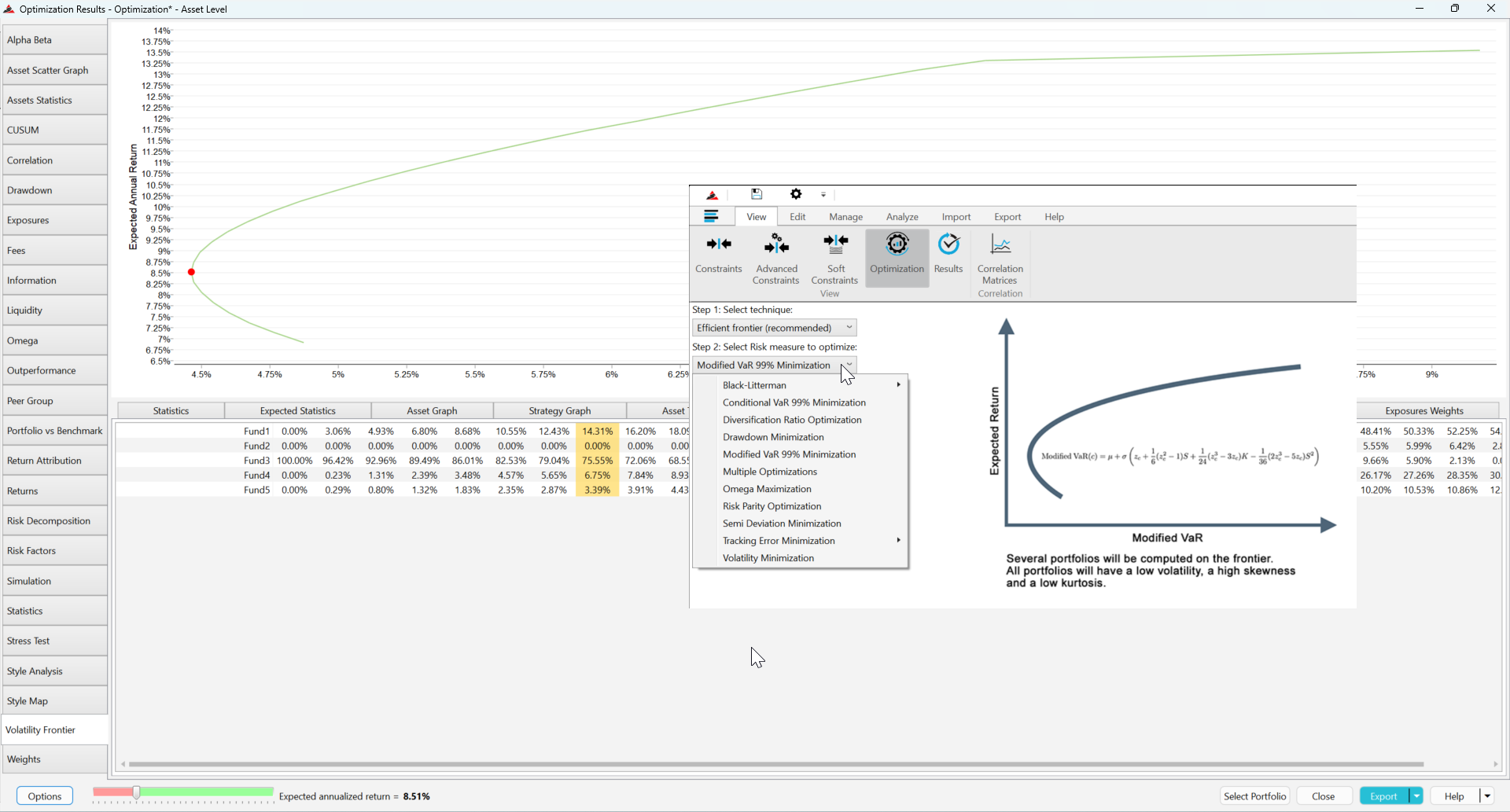

Markowitz efficient frontier with full constraint support - min/max weights, sector limits, liquidity constraints and factor exposure bounds.

Equal risk contribution and risk budgeting approaches. Allocate by risk rather than capital for more balanced portfolio construction.

Incorporate manager views and market expectations into the optimisation process - blending quantitative models with qualitative judgement.

AlternativeSoft's optimisation engine handles the complexity of alternative investments - including illiquid assets, lock-up constraints and non-normal return distributions - producing robust, implementable portfolios.

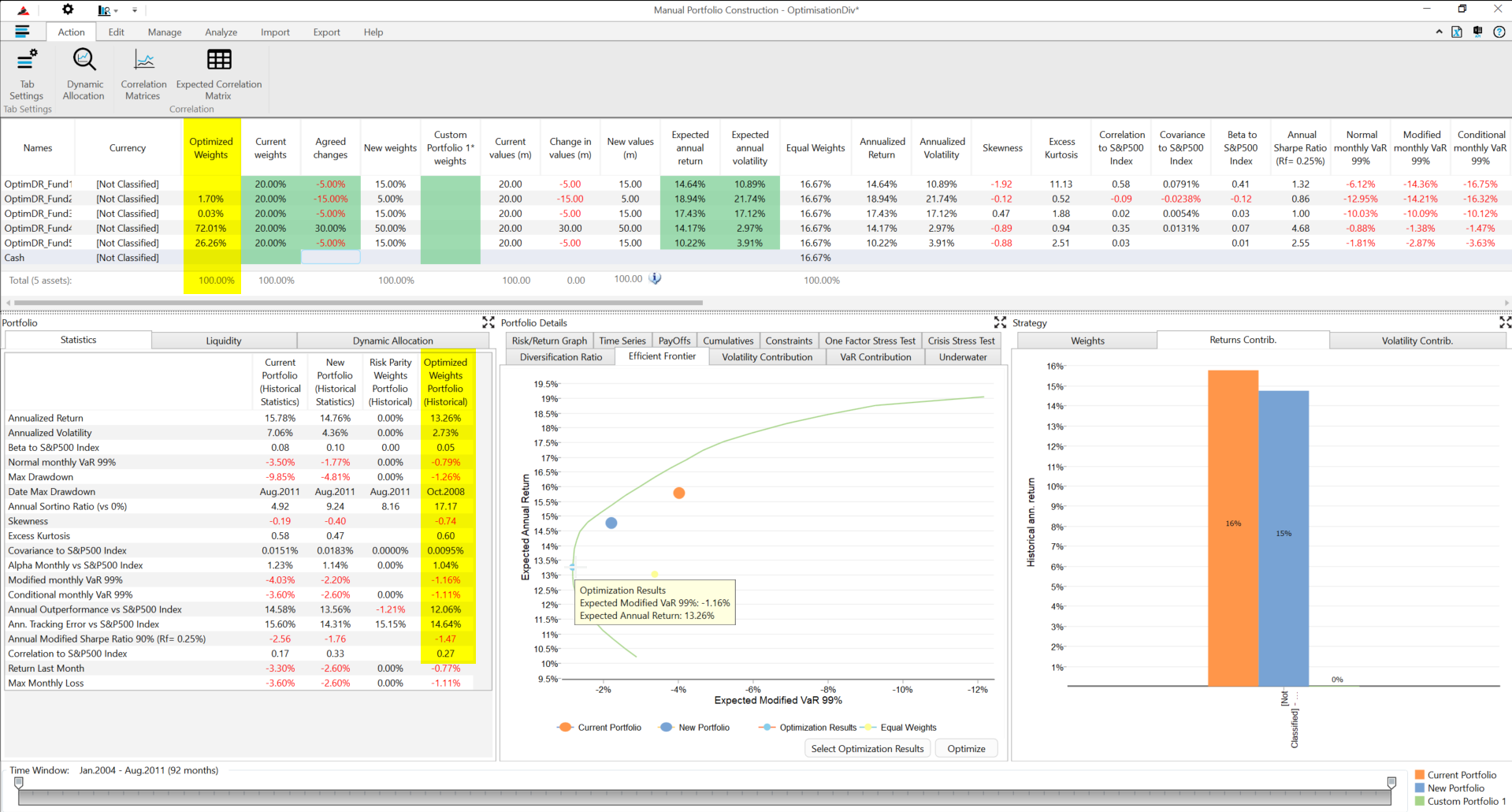

Once optimised, AlternativeSoft tracks actual portfolio performance against the optimised target - identifying drift, measuring attribution and supporting rebalancing decisions.

AlternativeSoft streamlines many useful performance-based analytics including portfolio optimisation, peer evaluation and relative analyses. One of the easiest softwares for portfolio what-if and customised fund fact sheets I have ever handled.

AlternativeSoft is a practical and user-friendly tool used as part of our portfolio construction and risk management process. Their extensive support and responsiveness provides added value.

From statistical analysis on a single hedge fund, screening the investment universe, peer group analysis, portfolio construction to risk analysis and stress testing - one of the most effective, intuitive, and efficient tools I have handled.

Join 150+ institutional investors. Book a personalised demo tailored to your needs today.

We'll respond within one business day.