Institutional-grade tools to design, stress test and optimise complex multi-manager portfolios.

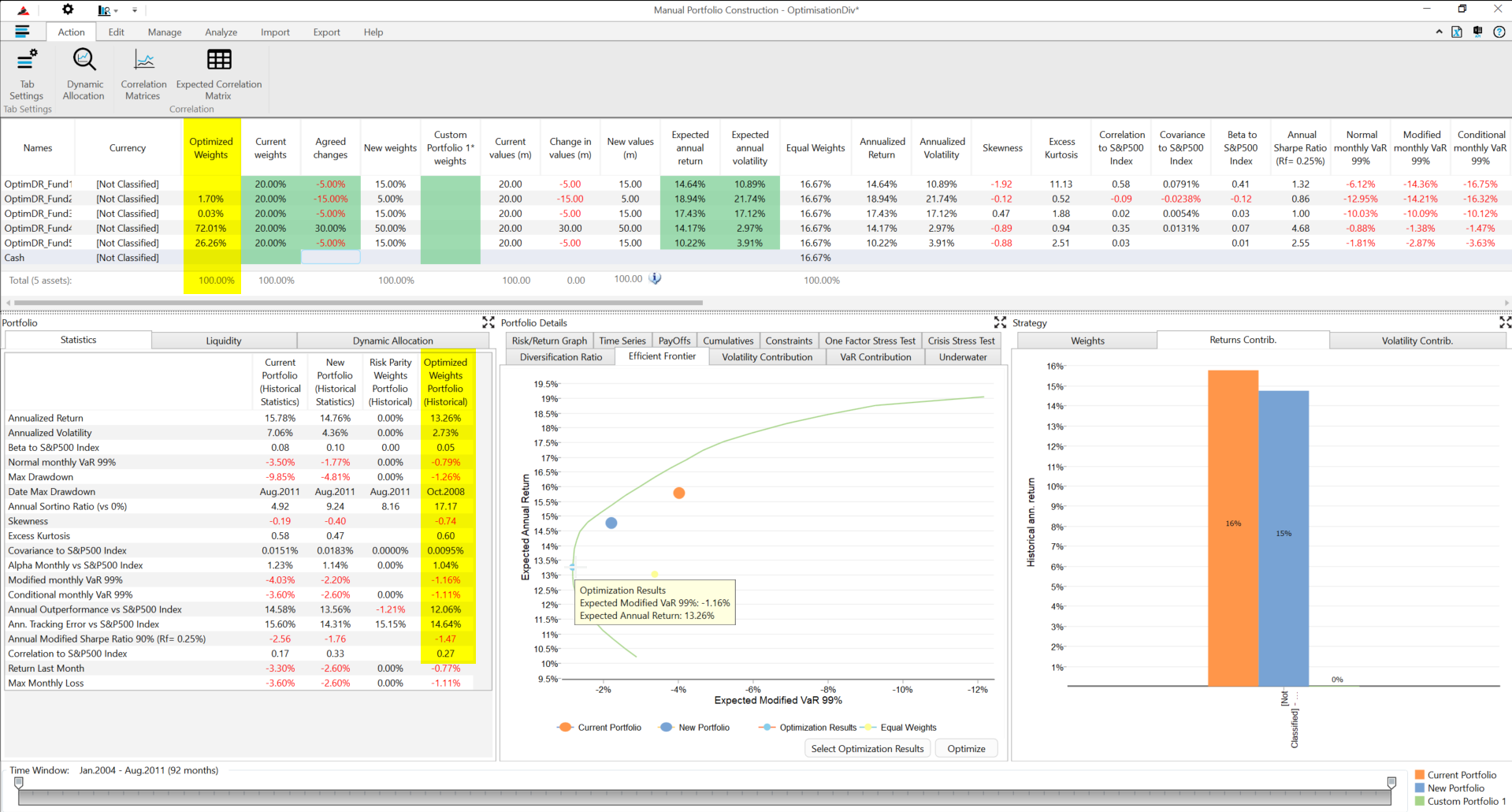

Map the risk-return efficient frontier across all available funds. Identify the optimal allocation to maximise return for any given level of risk.

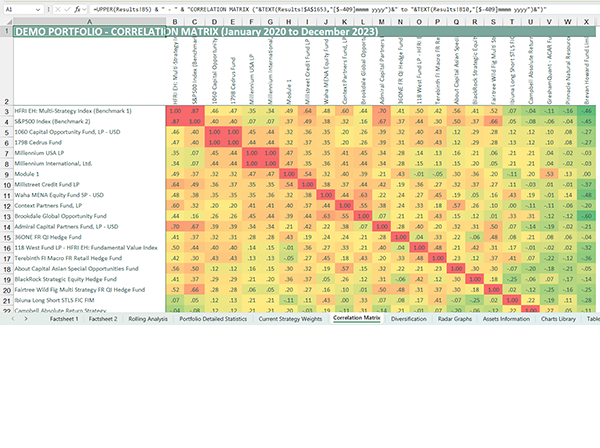

Mean-variance, risk parity, minimum variance and Black-Litterman optimisation - with full support for alternative assets.

Simulate portfolio performance across market scenarios before deploying capital. Test resilience against historical crises and custom shocks.

AlternativeSoft's portfolio construction engine supports every major optimisation methodology - from classic mean-variance to risk parity and factor-constrained approaches - across hedge funds, private markets and liquid alternatives.

Before allocating capital, simulate the impact on portfolio risk and return. AlternativeSoft's what-if engine lets you test new fund additions, position size changes and rebalancing strategies interactively.

AlternativeSoft streamlines many useful performance-based analytics including portfolio optimisation, peer evaluation and relative analyses. One of the easiest softwares for portfolio what-if and customised fund fact sheets I have ever handled.

AlternativeSoft is a practical and user-friendly tool used as part of our portfolio construction and risk management process. Their extensive support and responsiveness provides added value.

From statistical analysis on a single hedge fund, screening the investment universe, peer group analysis, portfolio construction to risk analysis and stress testing - one of the most effective, intuitive, and efficient tools I have handled.

Join 150+ institutional investors. Book a personalised demo tailored to your needs today.

We'll respond within one business day.