- Mon - Fri 8:00 - 19:00 GMT

- UK: +44 (0)20 7510 2003 | USA: +1 630 632 5777

- information@alternativesoft.com

- Trusted by640+ Users

- Best Risk management Software2023 | 2022 | 2021 | 2020

At AlternativeSoft, we are dedicated to safeguarding your data and ensuring the highest levels of security and compliance. We are proud to announce that we have achieved SOC 2 (System and Organization Controls 2) certification, a significant milestone that underscores our commitment to your data's safety.

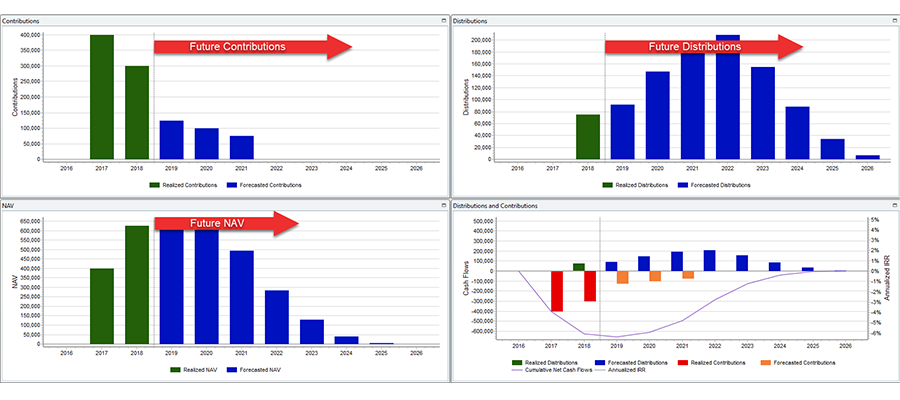

Our clients are now able to manage a hedge funds and private equity funds’ portfolio using contributions and distributions.

Find out why some of the world’s largest pension funds, fund of funds, family offices, private banks, endowments, foundations, wealth managers and advisers trust AlternativeSoft to identify and analyse multi-asset class portfolios of hedge funds, mutual funds, ETFs and private market funds.

Recently, a critical vulnerability in source code Log4j has impacted some companies worldwide. We want to ensure all our clients that our products and solutions do not use Java or Log4j library. All client data remains safe and secure.

This new feature helps our clients easily explore the User Manual, access the Video training guides as well as look through the FAQs. In addition, it also allows our clients to book 1 on 1 meetings though the Webinar Training.

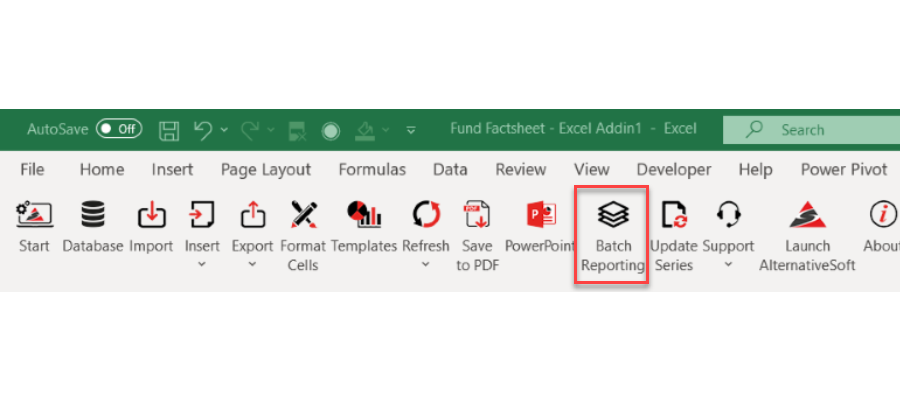

This features allows you to create batch reports, in Powerpoint format, using the Active worksheet as a template. As a result clients can now export their custom reports to Powerpoint quickly and easily.

Due diligence can be exceptionally time-consuming, when you have to deal with the collection of returns, estimates, weights, documents and questionnaires.

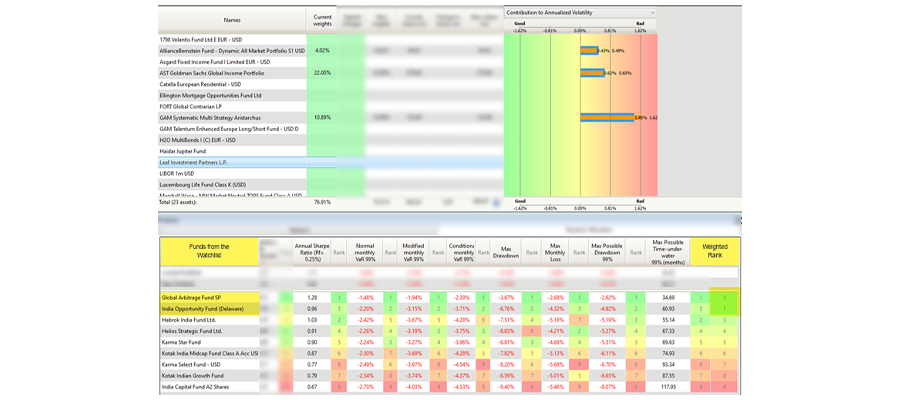

Using the new feature, clients can select up to 10 funds and control which specific funds improve performance in terms of portfolio statistics such as return, volatility, drawdown, maximum monthly loss or VaR.

We are proud announce that it now supports NilssonHedge Fund data as a free data set for our clients on our desktop and cloud based solution.

We are proud to introduce our new cloud based application AlternativeSoft Due Diligence Exchange.

AlternativeSoft are proud to announce our latest new features for our Private Equity module.

Type a Fund Name among our aggregated database of over 150,000 funds and visualize that funds extreme risks and see which other funds have consistently better returns within the same strategy.

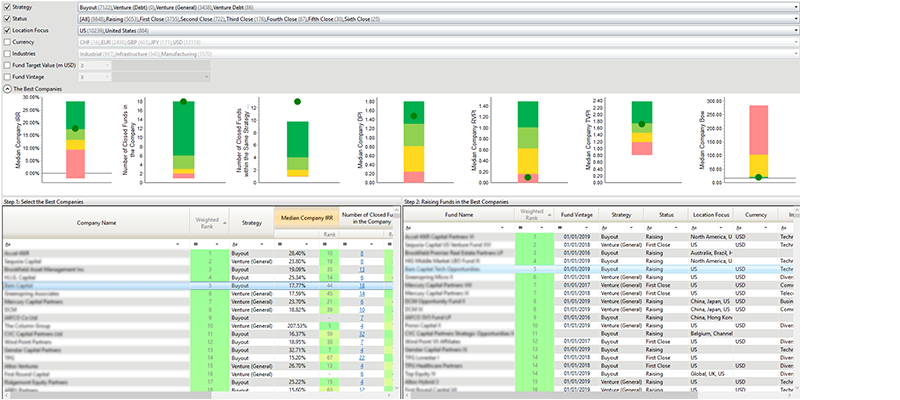

AlternativeSoft has implemented the Yale model in the Private Equity Module of AlternativeSoft. This allows Private Equity investors to easily define the return they expect from their investment in a Private Equity fund.

In today's dynamic financial landscape, traditional investment avenues may not always yield the desired returns. Savvy investors are increasingly turning to alternative investments to diversify their portfolios and enhance performance. As the demand for these non-traditional assets grows, the need for sophisticated analytics platforms becomes paramount.

In the rapidly evolving landscape of finance, mastering your investments requires more than just intuition; it demands a data-driven approach powered by cutting-edge technology. This comprehensive guide explores the transformative role of investment analytics tools in optimizing portfolios, mitigating risks, and achieving superior returns.

In an era of rapid technological advancements, the landscape of pension fund management is undergoing a transformative shift. As individuals plan for their retirement, it becomes increasingly essential to embrace innovative tools and strategies that can ensure the long-term sustainability and growth of pension funds.

In an era where data reigns supreme, the world of private wealth management is undergoing a transformative shift. Traditional approaches are giving way to innovative solutions that harness the power of data analytics to inform critical investment decisions. The rise of Private Wealth Management Software, with AlternativeSoft at the forefront, is reshaping the landscape, allowing wealth managers to seamlessly navigate complex markets and empower their clients with insightful decision-making tools.

Impact investing has gained significant traction in recent years as investors seek not only financial returns but also positive social and environmental outcomes. As individuals and institutions increasingly align their investments with their values, understanding the performance metrics of impact investments becomes crucial.

In the dynamic world of finance, making informed investment decisions is crucial for success. As investors seek ways to maximize returns while aligning with sustainable and impactful strategies, the role of portfolio analysis tools becomes increasingly significant. In this blog, we'll explore the importance of mastering investment insights through a deep dive into portfolio analysis tools, with a spotlight on how AlternativeSoft is contributing to this transformative landscape.

In the ever-evolving landscape of finance, staying ahead of regulatory requirements is crucial for success. This is where Investment Compliance Software plays a pivotal role, enabling investors to navigate complex regulations seamlessly and optimize their strategies. One prominent player in this space is AlternativeSoft, revolutionizing the way investment performance is impacted and strategies are transformed.

Within the dynamic realm of financial management, private wealth management stands out as a crucial element in securing financial prosperity for high-net-worth individuals and families. As financial portfolios grow in complexity and the demand for immediate insights intensifies, the importance of private wealth management software has reached unprecedented levels.

The integration of Environmental, Social, and Governance (ESG) principles into endowment management heralds a new era of investing. Explore how sustainable investing aligns with financial goals while fostering positive societal and environmental change, redefining the role of endowments in creating a sustainable future.

For family offices entrusted with safeguarding generational wealth, effective risk management is paramount. Explore comprehensive strategies and methodologies designed to shield wealth from potential risks while ensuring its preservation and growth across multiple generations.

Investment due diligence forms the bedrock of sound financial decision-making for a spectrum of institutions—from endowments and pension funds to hedge funds and wealth managers. Discover a comprehensive framework that streamlines operational due diligence, offering a roadmap for informed investment decisions across various sectors.

In the unpredictable world of finance, market volatility is a reality. For hedge funds, mastering strategies during these uncertain times is key to success. Explore the proactive approaches and tactical maneuvers that hedge funds can employ to not just survive but thrive amidst market turbulence.

Private equity continues to evolve, adapting to new market dynamics and opportunities. Delve into the latest trends shaping the private equity landscape in 2023, uncovering emerging strategies, sectors of interest, and the impact of market shifts on investment decisions.

Hedge fund managers operate in a dynamic and competitive industry. To achieve success, it's vital to employ effective strategies that set you apart. In this blog post, we'll explore key strategies and insights for hedge fund managers to navigate growth and achieve long-term success.

In an era of economic uncertainty, pension funds face a unique set of challenges. To ensure the financial security of retirees, pension fund managers must navigate volatile markets while delivering consistent returns. In this blog post, we will explore the key considerations and strategies to maximize returns for pension funds.

The investment landscape is evolving. As an increasing number of Family Offices and other institutional investors seek to optimize their portfolio management strategies, many are turning to artificial intelligence (AI) as a powerful tool for achieving superior performance.

Hedge fund managers operate in a dynamic and competitive industry. To achieve success, it's vital to employ effective strategies that set you apart. In this blog post, we'll explore key strategies and insights for hedge fund managers to navigate growth and achieve long-term success.

Family offices operate at the intersection of wealth management, investments, and legacy planning. Discover how cutting-edge software solutions can streamline operations, enhance performance, and safeguard your family's financial future.

Endowments serve as financial pillars for institutions, supporting long-term goals and sustainability. Explore how advanced software solutions can optimize investment management for endowments, ensuring their continued growth and impact.

Successful fund management begins with rigorous due diligence. Explore the best practices that underpin informed decision-making, risk management, and the pursuit of superior returns.

Institutional investors play a pivotal role in the world of finance. Delve into the strategies and insights that drive success for institutions managing large portfolios.

In the digital age of finance, data is the lifeblood of informed decisions. Explore the world of data aggregators and how they revolutionize the way financial information is gathered, analyzed, and utilized.

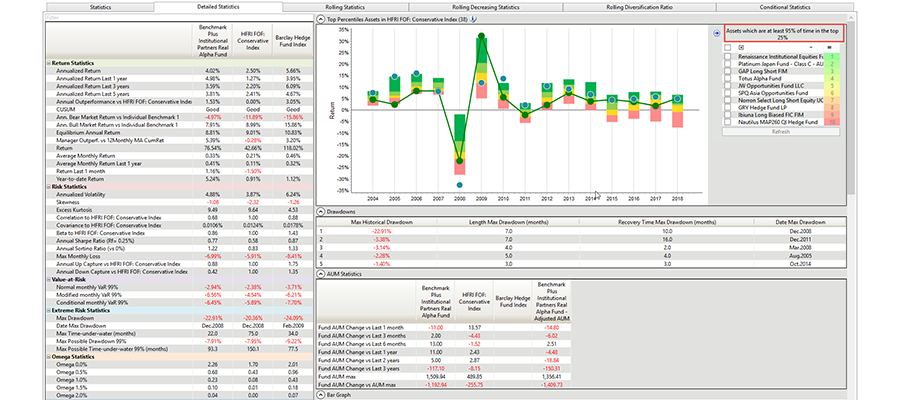

Unlock the power of regression analysis in understanding and managing hedge fund exposures. Explore how this analytical technique can provide valuable insights into your investment portfolio.

In the realm of alternative investments, the lines between private equity and hedge funds can be blurred. Dive deep into their differences to make informed investment decisions.

In today's data-driven world of finance, the right software can be your most valuable asset. Explore cutting-edge solutions that empower you to optimize your investment management processes.

Diversification is the cornerstone of a resilient investment strategy. Explore our selection of top alternative funds that can help you diversify your portfolio and manage risk.

In the world of hedge fund investments, access to information is paramount. Explore our free hedge fund database – a valuable resource to empower your investment decisions.

The Sharpe Ratio is a fundamental tool for assessing the risk-adjusted return of your investments. Dive into this essential metric, demystify its equation, and elevate your understanding of portfolio performance.

When it comes to evaluating hedge funds and alternative investments, the AIMA Due Diligence Questionnaire is an invaluable tool. Discover its significance and how it can shape your investment decisions.

Are you considering hedge fund investments? Navigating the intricate landscape of alternative investments can be a challenging endeavor. That's where our Hedge Fund Consultancy services come in.

In today's dynamic investment landscape, managing your private equity portfolio demands precision and efficiency. Discover the transformative power of Private Equity Portfolio Management Software at AlternativeSoft.

When it comes to evaluating hedge funds and alternative investments, the AIMA Due Diligence Questionnaire is an invaluable tool. Discover its significance and how it can shape your investment decisions.

Investment management solutions have changed the way investment managers manage their portfolios, but software tools like these aren’t always straightforward to implement and start using. This is where the value-add of post-sales support becomes crucial to successful solution adoption.

In fund Investing, the volume of data you need to access, manage and analyse can become overwhelming. And as your client base grows, managing portfolios becomes increasingly complex and prone to error. Discover how AlternativeSoft's scalable portfolio analytics solutions can help you to manage your data and processes at pace, efficiently and confidently.

Post the 2008 financial crisis, regulatory requirements regarding operational efficiency have become more stringent, resulting in an increased focus from firms on their operational due diligence. Operational due diligence is the process by which investors evaluate how an investment firm is managed, and whether the firm’s personnel can be trusted to manage the firm for the benefit of its investors, not just its managers.

The challenges associated with effective manager allocation can be complex enough to allocators without onerous due diligence obligations. And with the ever-changing industry and regulatory ecosystem, conducting due diligence confidently is becoming increasingly difficult. This is where effective digital due diligence solutions can help.

This article explores the challenges associated with managing risk and how fund investors and firms can benefit from comprehensive risk management solutions to effectively manage current and future risk, ensuring processes are as future-proofed as possible.

The adoption and use of cloud computing has become more and more prevalent in recent years, and providers of financial-technology solutions are increasingly offering cloud-hosted versions of their software to customers.

Fund managers and allocators have become increasingly aware of operational risk and the need to transform their operational due diligence process to account for changing compliance expectations.

This remarkable achievement wouldn't have been possible without the unwavering support and trust of our valued clients. Your confidence in us is our biggest motivation, and we are incredibly grateful for your ongoing support.

AlternativeSoft, a global provider of asset selection, operational due diligence, and portfolio construction solutions, has announced that Witherspoon, an asset manager who specializes in liquid alternative investments, has integrated AlternativeSoft’s Portfolio Construction module into its asset management platform, creating a powerful decision-making platform for alternatives

A good investment is one thing, but combining ideas and strategies for maximum return means constructing optimal portfolios. Portfolio construction can help you extract the maximum potential out of your investments, but if your portfolio construction process isn’t complemented with a flexible digital solution, you’ll end up spending more time, money and effort in the long run.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek European Awards for the forth time, marking our 9th award in 10 years, winning the award in back to back concessions!

Product selection, asset allocation, data leveraging and effective portfolio building are all constructive approaches to ensuring success against market volatility and evolving regulatory requirements. But risk, and effectively managing risk, has become of paramount importance in optimal fund management, with firms and fund managers honing in on the best practices and approaches to secure portfolios against the impacts of risk.

AlternativeSoft are excited to announce the appointment of Ayman Abouhend as Company Officer for Mergers and Growth, Christopher Demetropoulos, who joins in an advisory role as a board member and Steve Gollins as Head of Sales in North America.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek European Awards.

In light of the Coronavirus pandemic, we have decided to implement a work from home policy which has been robustly tested over the last few weeks.

We are excited to announce that our team has moved to a new location in Farringdon. 81 Farringdon Street, London, EC4A 4BL

Over the summer AlternativeSoft have been busy onboarded several large financial institutions.

AlternativeSoft users will gain free access to over 100 free global equity indices thanks to Morningstar’s Open Indexes Project.

Join AlternativeSoft in the first of our series of webinars on the best-performing hedge funds and mutual funds and tips for selecting funds that perform across all market conditions.

YTD year on year sales increase of 30% and expansion of our Sales, Support and Quantitative Teams which now takes our total head count to 35 as well as a new office.

AlternativeSoft hired and continues the expansion of its London office by boosting our existing Client Services team with 3 new faces!

We interviewed Don Steinbrugge from Agecroft Partners and asked him some questions regarding the economy, coronavirus and conferences.

After a difficult few months due to the pandemic, Year-to-date, only 4 hedge fund sectors were in the black for April, including....

S&P 500 index rose far above benchmark gauges in Asia.

As the Covid-19 pandemic shows the earliest signs of drawing to a close, there are split opinions among hedge funds regarding what the next move should be.

PE firms sitting on $1.5tn to be used for “market dislocation”

Millions sent home as 3 hedge funds still manage to outperform market sell-off

Many believe Platt is the highest earning person in finance

A Danish hedge fund by the name of Asgard Credit is shorting Tesla bonds

Is machine learning beginning to take centre stage?

Greg Jensen Co-CIO believes these 3 reasons will cause gold to rise

Conrad and Shilling’s top ten mutual funds list (With associated five-year returns)

Less than 9,000 hedge funds now exist globally

Singapore is home to two of the top ten HF in 2019

Airbus, Moody’s, Charter Communications and more have been warned by TCI

Fears grow as assets held by private equity firms grows 83% in past decade

Founder and Billionaire Ray Dalio takes to social media to contest WSJ

Top 10 most loved stocks from 833 top hedge funds

Money being left on the table for player likeness, use of names and more

Switching from a partnership to a corporation has served many private equity firms very well.

For most firms’ women hold just 1 or 2 of the top positions on the buyout investment teams

Secondary deals have already broken 42bn for the first semester of 2019

The European Central Bank has lowered its deposit rate by 10 basis points as Draghi looks to step down next month

Sorrell to take up a senior role at rival asset management firm

$400m for majority stake in one of India’s largest education service providers EuroKids

Two private equity companies are looking to co-own the makers of Norton Anti-Virus software

180% stake increase makes gold hedge funds biggest held position

Soaring temperatures leads to 60% increase in carbon-emissions credits

Some firms have raised billions to take general partner stakes in other private equity players.

Berlin based ratings company “Scope” found that Multi-asset funds that invest directly in securities outperformed fund-of-funds over a 10-year period.

Franklin Templeton and Hasenstab dividing global opinion with latest bet

Some firms have raised billions to take general partner stakes in other private equity players.

Top 5 buys and sells from the world’s biggest hedge funds

Traders have dumped riskier assets such as stocks and crude oil moving towards “safe havens assets” including bonds.

Reports of hedge funds pushing for brexit have been rubbished by multiple sources.

GPIF want to make the market more sustainable not beat it.

Gold has risen 18% this year making it a refuge for hedge funds.

ABG is critical first deal for BlackRock as they continue to fundraise with target of $12b for LTPC fund.

After the antics of Abraaj Group investors have been reluctant to seek other opportunities in this region of the world.

Funds which rely more on insider money outperform funds that use asset gathering.

Disney Plus, Hulu and ESPN for the same price as Netflix suggests direct attack.

Only one new hedge fund has managed to reach $2b this year, $6b shy of last year’s highest total.

Investors are gambling on further falls in share price.

Carlyle look to improve share price with inclusion in index tracker funds.

Sterling falls to 2 and half year low as no-deal Brexit becomes real possibility.

Society is on the precipice of major shifts in wealth, energy sources and morality, could ESG investing turn the heads of hedge fund managers?

85% loss of partners money after energy stocks have a tough year. Energy fund Equinox Energy has announced its plans to close their fund after 4 and a half years of torment losing 85% of their partners money.

Curious to learn more about what AlternativeSoft can offer Fund Managers and Allocators in this dynamic landscape? Don't miss the chance to schedule a meeting with us at ALTSME Dubai.

If you’re attending SIPUGday, don’t miss the chance to connect with us and explore innovative possibilities. Let’s make valuable connections and drive the future of finance together!

AlternativeSoft is delighted to be attending the latest IPEM Paris 2023, on the 18th - 20th September 2023 at the Westin Vendôme and the Jardin des Tuileries, Paris.

AlternativeSoft is delighted to be attending the latest AIM Summit London Edition, on the 13th - 14th April 2023 at the Four Seasons Hotel London, Ten Trinity Square.

AlternativeSoft is delighted to be sponsoring the latest Markets Group ALTSLA conference, on the 27th - 29th March 2023, in Los Angeles.

AlternativeSoft is delighted to be attending the latest Private Wealth Switzerland Forum Zurich, on the 14th December 2022, in Zurich, Switzerland.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by and meet Ben and James.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by and meet Steve and Ravi.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by and meet Steve and Dipesh.

To find out how AlternativeSoft's industry leading solutions are helping some of the world's largest Hedge Fund Allocators make better informed investment decisions stop by our booth and meet our team. For more information please contact us.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by and meet Alex and Scott.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by and meet Alex and Scott.

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by booth 102 and meet Alex and Scott.

AlternativeSoft is proud to be sponsoring the Best Singapore-Based Hedge Fund Award at the Eurekahedge Asian Hedge Fund Awards 2019 later this week.

Good luck to all of the nominees!

To learn more about how AlternativeSoft's award-winning solutions are helping some of the world's largest investors make smarter investment decisions, stop by booth 31 and meet Dominique, Alex and James.

To find out how AlternativeSoft's industry leading solutions are helping some of the world's largest Hedge Fund Allocators make better informed investment decisions stop by our booth and meet our team. For more information please contact us.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek European Awards.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek European Awards.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek Global Awards.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek Global Awards.

AlternativeSoft won the award for ‘Best Risk Management Software’ in the Hedgeweek USA Awards.

First place in the ‘Technology Provider for Risk Management’ category of Hedge Funds Review Service Provider Rankings.

First place in the ‘Technology Provider for Risk Management’ category of Hedge Funds Review Service Provider Rankings.

First place in the ‘Technology Provider for Risk Management’ category of Hedge Funds Review Service Provider Rankings.

Second place in the ‘Technology Provider for Risk Management’ category of Hedge Funds Review Service Provider Rankings.

UK: 10 Lower Thames Street,

London, EC3R 6AF

USA: 1 Mid America Plaza, Suite 3016

Oakbrook Terrace, IL 60181

UK: +44 20 7510 2003

USA: +1 630 632 5777